As the foreclosure crisis continues unabated, experts continue to trawl for solutions. There are mortgage modifications and principal write-downs. Some have called for a national foreclosure moratorium. States are loaning unemployed borrowers money so that they can continue making mortgage payments. Borrowers are suing lenders in a last-ditch attempt to avoid foreclosure. I’d like to add another potential solution to the list: reverse mortgages.

For those that are struggling to make payments on their primary mortgage and/or are facing foreclosure, a reverse mortgage would seem to represent an ideal fix. Under a reverse mortgage, you can cease making monthly payments immediately, and you are entitled to stay in your home until you pass away, as long as you continue paying property taxes and hazard insurance premiums.

However, there are a few stipulations. First, you must be older than 62 years old in order to obtain a reverse mortgage, which means that only a small portion of mortgage borrowers are even eligible. In addition, your home equity must exceed a certain percentage in order to be eligible (the exact percentage depends on your age and interest rates). That’s because the entire primary mortgage must be paid off upon obtaining a reverse mortgage as well as because the FHA limits the proportion of your property value that you can borrow against. Finally, since a substantial portion of the reverse mortgage proceeds are probably being used to retire your primary mortgage, your cash position probably won’t improve much. Given that your home equity will also decline over time, it is imperative that you have savings and other sources of cash that you can use to continue supporting yourself.

When contemplating using a reverse mortgage to repay your primary mortgage, it’s important to remember that you are merely swapping one form of debt for another. In other words, the reverse mortgage – just like the primary mortgage – ultimately needs to be repaid. The advantage is that you can repay the loan from the sale of your home (following the death of the primary borrower) and can continue to reside in the home in the interim. The disadvantage is that because reverse mortgages are always negatively amortizing (i.e interest compounds on top of interest), you might end up owing more over the life of the loan than if you had merely continued to make monthly payments on your primary mortgage.

In short, reverse mortgages are really most appropriate for borrowers that are having difficulty making monthly payments for their primary mortgages and that are opposed (for whatever reason) to moving into a less expensive home.

It is technically possible to obtain a reverse mortgage for the purposes of consolidating / repaying other debts. However, prospective reverse mortgage borrowers needs to fully understand the implications of doing so. Moreover, since it is only economical in certain situations, borrowers need to think critically about how such will impact their personal financial situations and whether there might be better alternatives.

On the surface, reverse mortgages would seem to be eminently suited for debt consolidation. For example, you could use a reverse mortgage to eliminate an existing primary mortgage. Basically, you will trade your monthly payments for one big balloon payment. Unlike a conventional mortgage – which involves greater scrutiny – reverse mortgages can be obtained for any reason, and the proceeds can be spent however the borrower wants. Moreover, the reverse mortgage will inherently eliminate the need to continue making monthly payments, since it needs to repaid only when the last primary borrower passes away or moves out. Finally, a reverse mortgage may carry a lower rate of interest than other types of consumer debt.

On the other hand, just because lenders allow borrowers to obtain reverse mortgages in order to achieve debt relief doesn’t mean they should actually be used for that purpose. Under a reverse mortgage, interest will continue to accumulate on top of interest to the extent that one’s entire home equity can be wiped out over the course of a decade or two (depending on the size of the loan). Some would consider that a reasonable trade-off for alleviating the burden of having to repay other debt, but it’s not necessarily an economical choice. In addition, when you factor in the annual insurance premiums and the fact that the reverse mortgage interest compounds on itself, the actual APR will probably be several per-cent higher than the nominal interest rate, further eliminating any financial impetus for consolidating debt.

Ultimately, it depends on the amount of existing debt, the corresponding interest rates, and one’s personal financial situation. If you have only a small amount of debt accumulating at a low rate of interest and a stable source of income, you should consider repaying the debt directly. Since reverse mortgages are negatively amortizing, obtaining one for even a modest amount can still rapidly erode your home equity.

If, on the other hand, the existing debt is relatively large and/or the interest rate is quite high, if making monthly payments is taxing your finances and the only way you can repay the debt is if you sell your home, then a reverse mortgage might be the only realistic solution to maintain solvency and stay in your home.

Just bear in mind that you will still have to find a way to continue paying property taxes and hazard insurance, as well as to maintain the property for as long as you reside there. Since you have already tapped your home equity, you will have to use personal savings and income to defray these costs. Unfortunately, if your personal finances are inadequate, you may have to consider selling your home and moving into a less expensive property. If need be, you can always obtain a reverse mortgage on that one instead.

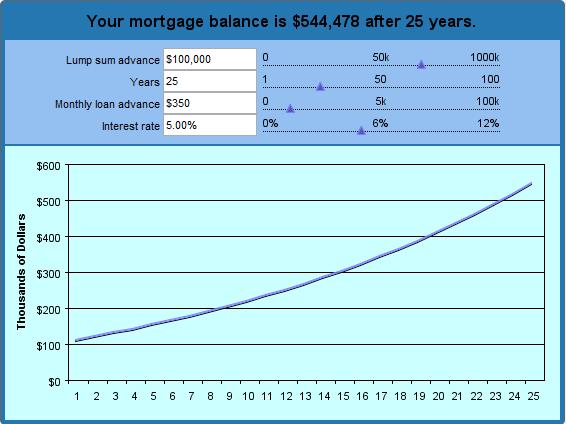

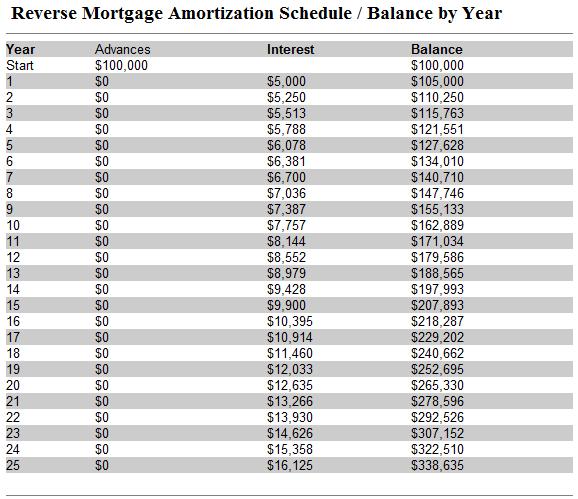

When you obtain a reverse mortgage, your lender should furnish you with – among other things – an amortization schedule, which is basically a table/graph of how the loan balance will change over time.

The amortization schedule for a reverse mortgage is unique because it is a negatively-amortizing loan. Since it is repaid all at one time only and (usually) only when the last primary borrower passes away, the loan balance for a reverse mortgage will increase over time. This contrasts with a conventional mortgage, the loan balance of which should decrease evenly over time and eventually disappear as a result of making monthly payments.

The best way to conceptualize this is to create a hypothetical amortization schedule even before you begin the process of shopping for a reverse mortgage. Using our reverse mortgage calculator, you can clearly see how your loan balance will increase (as interest and principal compound) until the reverse mortgage is repaid. Because you aren’t required to make monthly payments, the loan balance will grow exponentially, to the point that 15 years from now, it will accrue interest twice as fast as the current rate. 25 years from now, it will accrue interest 3 times as fast.

In the sample above, I keyed in a lump sum advance of $100,000 and term payments of $350 per month. I assumed an interest rate of 5% and requested a 25-year chart. (In other words, if I obtain a reverse mortgage at the age of 62, when I first become eligible, I can see how much I will owe by the time I am 87. Based on these parameters, the calculator determined that I will receive a total of $190,000 (lump-sum advance + cumulative monthly payments). Over this time, the loan will accrue $325,072 in interest, which means that the lender will be owed $515,072. Wow!

While you can adjust the parameters as you see fit, you should bear in mind a couple things. First, the actual interest rate (APR) will be even higher when you take into account closing costs and FHA insurance premiums. Second, this insurance protects you from owing more on your reverse mortgage than your home is worth (a real possibility if you stay in your home long enough), which means that the loan balance on an FHA-insured loan is only relevant insofar as you (or your heirs) ultimately intend to keep your house and pay off the reverse mortgage in cash.

With mortgage rates at record lows, many borrowers have moved to refinance their mortgages. Some have even refinanced multiple times over the last few years. Given that closing costs (for all mortgages) are rising and that refinancing often extends the duration of one’s mortgage, it might ultimately be more economical to obtain a reverse mortgage.

Consider that a refinancing could cost you 3-5% of the value of your home. Whether the fees are paid up-front or rolled into the loan balance, a refinancing is expensive. Of course, the idea is that you will reduce your monthly payment and/or save money in interest charges over the life of the loan, and you would be foolish to refinance unless you could achieve at least one of these outcomes.

If you are already retired and/or eligible for a reverse mortgage, why not re-apply the cash that you would have to pay upfront for a refinancing towards obtaining a reverse mortgage instead. Surprisingly (given that reverse mortgages are often lambasted for their high costs), the cost of obtaining a reverse mortgage may in fact be cheaper than going through the process of refinancing. For example, the recently introduced Home Equity Conversion Mortgage (HECM) Saver eliminated the upfront FHA insurance premium, which was the largest upfront cost for most reverse mortgage borrowers. As if that weren’t enough, many lenders offer additional financial incentives to borrowers, such as no-closing cost loans.

In addition, while reverse mortgage rates aren’t as low as mortgage rates (due to an FHA rate floor), there is a good chance that they are lower than the interest rate attached to your current mortgage, especially if you are contemplating a refinance. Not only that, but the nature of reverse mortgages is such that the flow of funds will be reversed. Instead of making a (smaller) mortgage payment every month, you will receive a (relative to when interest rates were higher) larger one. The two main offsets to savings are the annual insurance premiums and the fact that your reverse mortgage negatively amortizes, meaning the balance will increase over time.

On some level, it’s ridiculous to compare a reverse mortgage with a refinanced mortgage, since the two are fundamentally different. At the same time, the decision behind both stems from a common motivation to save money on one’s mortgage. In short, the greatest savings can probably be achieved by refinancing, but you can reshape your financial situation, alter your monthly income stream, and eliminate the burden of monthly payments altogether by instead obtaining a reverse mortgage.

Be sure to read my complete overview of the financial and non-financial pros and cons of reverse mortgages for more guidance on making this decision.

Having made the decision to obtain an HECM reverse mortgage, many prospective borrowers deliberately do not shop around. They figure that because it’s a standardized product insured by a government agency, therefore every lender must offer identical terms at identical rates. In fact, nothing could be further from the truth. No Closing Cost Reverse Mortgages represent a case in point.

In response to charges that due to high upfront costs, reverse mortgages were prohibitively expensive, many lenders engaged in a conscious effort to lower the costs. Given that an interest rate floor is determined by the FHA, there was/is only so much they could do. In some cases, they paid the upfront insurance premium for borrowers. In other cases, they eliminated their origination fees. Still other lenders agreed to pay certain third party closing costs on behalf of borrowers.

Of course, lenders must have some kind of financial incentive for reducing costs, especially since the industry has not (yet) collectively resolved to lower costs together. In fact, some lenders stipulate that they will only waive their closing costs if the loan amount exceeds a certain value. No Closing Cost proprietary reverse mortgages are especially likely to contain such terms. Instead, they might require borrowers to roll the savings into the reverse mortgage, and/or take all of the cash upfront. Then again, it’s easy for lenders to manage the risk with reverse mortgages (especially given the majority are FHA-insured), and profits from interest are more than enough to offset lost revenue from lower upfront costs.

A few years ago, a handful of pioneering lenders led the way in cutting their closing costs. While the collapse of the housing bubble spurred a reassessment of risk management practices, many lenders are once again examining how they can be more competitive. Especially since the HECM Saver (which doesn’t carry an upfront insurance premium) was introduced, lenders have little choice but to reduce closing costs if they want to offer a less expensive product.

In short, before committing to a specific lender, make sure you do some research. Even if you have already applied and are waist-deep in the process, it doesn’t hurt to ask your lender for a discount. Remember that until you sign the mortgage contract (and even then you still have a 3-Day Right of Rescission), you are under no obligation to obtain the reverse mortgage. Make sure you take advantage of that freedom to obtain the best terms/rates that are available.

It now seems that the Guidance issued recently by the Federal Financial Institutions Examination Council (FFIEC) was a mere prelude to actual regulatory changes. In August 2010, the Federal Reserve Bank proposed “enhanced consumer protections and disclosures” for reverse mortgages. Now, the 90-day comment period that followed its publication is about to expire, and following some additional revisions, the Fed’s proposals could become tantamount to law.

The Fed’s overarching goal is to improve the disclosures that borrowers receive at various stages throughout the reverse mortgage. (The Fed will also push to strengthen regulations governing the marketing of reverse mortgages, to further limit lenders from cross-selling other financial products in conjunction with reverse mortgages, and to clarify the borrower’s Right to Rescind, but these are all subsumed under the umbrella of disclosure).

Under the proposed changes, prospective borrowers “would receive disclosure on or with the application form, using simple language to highlight the basic features and risks of reverse mortgages.” The purpose of this initial disclosure would be to clarify how reverse mortgages are different from conventional mortgages. After receiving the application, lenders would be required to furnish “transaction-specific disclosures that reflect the actual terms of the reverse mortgage being offered.”

The sample disclosure form prepared by the Fed is both comprehensive and specific. It first lists information about the borrower and property, followed by a basic description of the reverse mortgage, including the borrower’s rights and responsibilities. The next section details the disbursement of funds and informs the borrower that he may change the form of disbursement (from line of credit to monthly advance, for example). This is followed by an explanation of APR, including how it is determined and whether it can change.

Next is a discussion of fees, beginning with origination fees (“Account Opening Fees”), and followed by monthly service fees and any early termination fees. After a brief summary of borrowing guidelines and limits, there is a table that shows how the loan balance will (hypothetically) grow over time. Repayment options are covered, as are the risks. Here, lenders explicate the conditions under which they would cease disbursement of funds, terminate the loan, and/or foreclose on the property. Finally, there is some boiler-plate language stating that the prospective borrower is under no obligation to accept the terms of the reverse mortgage, that he has the right to rescind the loan, and that he should seek counseling before taking further action.

While the fed acknowledges that “disclosures alone may not always be sufficient to protect consumers from unfair practices related to reverse mortgages,” it is nonetheless agreed that better disclosure will at least serve to stop borrowers from obtaining them without fully understanding what they are getting themselves into.

Due to its unique structure, a reverse mortgage can be obtained without any examination of the borrower’s creditworthiness. Instead, lenders will focus on the quality of the home, which serves as collateral for the loan. However, there is evidence that this could soon change, and that lenders could begin conducting credit checks for prospective borrowers.

In fact, it is already the case that proprietary reverse mortgage loans require borrowers to have strong credit. That’s not because proprietary loans are structured differently from FHA-insured Home Equity Conversion Mortgages (HECM), the product of choice for 95% of reverse mortgage borrowers. Instead, lenders merely need confirmation that borrowers have the means to pay property taxes, hazard insurance premiums, and maintain their properties, thereby mitigating any possibility of default.

With HECM reverse mortgages, this is not of primary concern to lenders. To be sure, default/foreclosure is always unfortunate, and it is an undesirable outcome for all parties involved. However, the fact that HECM loans are insured by the FHA means that lenders don’t need to worry about what would happen in the event of default, since any losses will be defrayed by the FHA. With proprietary loans, in contrast, all losses are absorbed directly by lenders, or by investors in reverse mortgage backed securities.

Given that default is inherently undesirable, the reverse mortgage industry is currently brainstorming solutions designed to prevent it from happening. One proposal is that when the reverse mortgage is originated, an escrow account will be created, so that property taxes and hazard insurance premiums can be paid automatically. In fact, escrow accounts are required for many conventional mortgages, and it’s unclear why they were never deemed necessary for reverse mortgages. Another proposal would mirror the steps taken by proprietary lenders. By performing a simple credit check, lenders can quickly screen potential borrowers and reject those that are most likely to default.

This is important if reverse mortgages are to continue their push into the mainstream. With even lower rates of default, reverse mortgages will become even more attractive to investors and better candidates for securitization. That should lead to the lowering of reverse mortgage interest rates and generally more attractive terms for borrowers. One day, proprietary reverse mortgages might even hope to rival HECM reverse mortgages in popularity.

For now, most borrowers can rest assured that their credit history – whether strong or weak – is not a factor in their reverse mortgage application. As for whether this will be the case in the future, well, we will have to wait and see.

The FHA-insured Home Equity Conversion Mortgage (HECM) is the product of choice for the overwhelming majority of reverse mortgage borrowers. However, the current loan maximum for both the HECM standard and HECM Saver is $625,500, which means that those with more expensive homes must utilize Jumbo loans for their reverse mortgage needs.

Jumbo reverse mortgages are a form of proprietary mortgages, and must necessarily be obtained directly from the lender. On the one hand, the absence of FHA insurance premiums eliminates one of the most significant costs for borrowers. On the other hand, this also removes the main safety feature of reverse mortgages, and besides, lenders will always compensate for the lack of insurance by charging a higher interest rate. They will also require a solid credit history, in order to ensure that borrowers have the means to pay taxes and hazard insurance premiums, as well as to maintain the property, after the reverse mortgage has been originated.

Even though proprietary reverse mortgages are not subject to the same standards as HECM reverse mortgages, they are becoming subject to increasingly stringent regulation. A handful of states have already legislated that all reverse mortgages conform to the same set of standards, including that proprietary mortgages must install the same safeguards to minimize the chance of default. Recent federal guidance, while non-binding, was also aimed at bringing proprietary reverse mortgages up to code.

Prior to the housing market crash, most major reverse mortgage lenders also offered a proprietary Jumbo product. As of November 2010, however, Generation Mortgage is the only such lender. Its Generation Plus Loan “targets owners over age 62 with homes appraising between $500,000 and $6 million,” and “carries a fixed rate of 7.78 or 8.78 percent, depending upon the program. All funds must be taken at closing. A minimum FICO score of 700 is required.” As the mortgage industry normalizes and securitization (in the form of Mortgage Backed Securities) becomes viable, the number of lenders offering proprietary reverse mortgage products should increase.

In addition, pending federal legislation would increase the loan limits in certain regions for all FHA borrowers, perhaps as high as $778,000 in the most expensive markets. In that case, a larger chunk of borrowers would become eligible for HECM reverse mortgages. However, given that it was only recently that the FHA’s dire financial circumstances prompted it to consider cutting limits, it seems unlikely that such legislation will be passed anytime soon. In reality, HECM reverse mortgage limits are just as likely to be lowered (to the former level of $417,000, or even lower) as they are to rise.

I recently reported on the Formal Guidance that the Federal Financial Institutions Examination Council (FFIEC) issued on the reverse mortgage industry. With this post, I want to focus on one section of the guidance: “Communications with Consumers.”

One of the main complaints about reverse mortgages is not with the product itself, but rather the way in which it is presented to consumers. Misleading ads claim that reverse mortgages are a government benefit, or that reverse mortgages are free, or that they don’t need to be repaid, or that they are structured in such a way that it is impossible to lose your home.

It seems that some prospective borrowers don’t learn the truth until they are knee-deep in the process and undergo the required counseling session. By this stage, the decision to obtain the reverse mortgage has already been made, which is why the FFIEC has encouraged the reverse mortgage industry to level with consumers, “from the moment a consumer begins shopping for a loan to the time a loan is closed…not just upon the submission of an application or at consummation.”

First, lenders need to make clear to consumers the fees and costs associated with the reverse mortgage, including origination fees, insurance premiums, other upfront third-party fees, interest costs, service fee set aside (“sfsa”), etc. It should be clearly explained that even though the borrower is not required to pay for any of these costs in cash, they are rolled into the reverse mortgage and are subtracted from the borrower’s home equity. Hence, they are not free and unless stated otherwise, they are defrayed directly by the borrower and not by the lender.

Next, lenders have a responsibility to explain the structure of reverse mortgages in a way that demystifies it. For example, borrowers should understand the different types of reverse mortgages available to them, as well as the terms and other features particular to each type. They need to further understand how the principal limits are calculated, “based on home value, borrower age, expected interest rates, and program limitations,” but that they are NOT required to borrow the maximum allowable amount. Lenders, meanwhile, should delineate the different options for disbursement of the reverse mortgage proceeds, including lump-sum payment, line of credit, term, and tenure.

Last and certainly not least, lenders need to clearly outline the risks of reverse mortgages and the obligations of borrowers. Most important are the conditions that would trigger a default, such as failure to pay taxes and hazard insurance, inability to maintain the property, or moving out. The borrower should understand unequivocally that the reverse mortgage must be repaid, as well as the process for doing so.

If all of the above guidelines are followed, accusations of false marketing would all but disappear. While some critics will continue to harp on the inappropriateness of reverse mortgages, at least they will have no cause to be angry with lenders. Borrowers will be able to make informed decisions, and those that regret their choice will sadly have only themselves to blame.

Last year, I offered a primer on Selecting a Reverse Mortgage Interest Rate. I want to update that post below, in accordance with the unveiling of the new HECM Saver, which differs from the existing HECM Standard in that it waives the upfront Insurance Premium in exchanging for lending smaller amounts to reverse mortgage borrowers.

The basic difference between fixed rates and variable rates is that the former stay the same throughout the life of the reverse mortgage, while the latter fluctuate. In a nutshell, the advantage of choosing a fixed rate is that it is stable and predictable, while a variable rate might offer the possibility of either short-term or long-term savings. As fixed rates are presently much higher than variable rates, you can think of a fixed-rate as a kind of security premium that you pay for not having to worry about rising interest rates.

It’s important to be aware that with a fixed-rate reverse mortgage, you will probably be required to receive the entire loan as an upfront payout. (That’s not to say that you can’t select a variable rate and an upfront payout). If you are determined to receive a line of credit or tenure/term monthly payments, you must accept a variable interest rate and the accompanying uncertainty.

As of November 2010, a fixed-rate HECM Standard can be obtained for 4.99%, while an HECM Saver can be obtained for 5.25%. (While conventional mortgage fixed-rates are slightly lower, a rate floor is dictated the FHA). Variable rates follow the same relationship; lenders might use the same benchmark interest rate (1-month LIBOR or a short-term Treasury rate), but will typically add a greater margin onto HECM Saver loans. Currently, an HECM Standard carries a variable rate of 2.5%, while an HECM Saver will carry a variable rate closer to 3%.

Regardless of whether you choose a fixed-rate or variable rate, any savings from not having to pay an upfront insurance premium (with the HECM Saver) might be offset by a higher interest rate. To make matter even more confusing, unused funds (if you select the line-of-credit payout option) will pay you interest at a higher rate with an HECM Saver, compared to an HECM Standard.

In short, choosing between a Saver and a Standard depends on how you withdraw the proceeds of the reverse mortgage and the planned duration of your reverse mortgage. The same is largely true when comparing fixed rates and variable rates. If you have a short time horizon, you will probably save money with a variable-rate HECM Saver. Since interest rates will probably rise within the next five years, however, those that plan to maintain the reverse mortgage indefinitely will probably come out ahead with a fixed-rate HECM Standard.