As I reported in my previous post, reverse mortgage lending volume has been shrinking and would appear to be trouble. As a new report by the National Association of Home Builders (NAHB) and MetLife points out, however, this could be about change. to Within the next couple decades, a handful of demographic drivers could spur fresh demand for reverse mortgages.

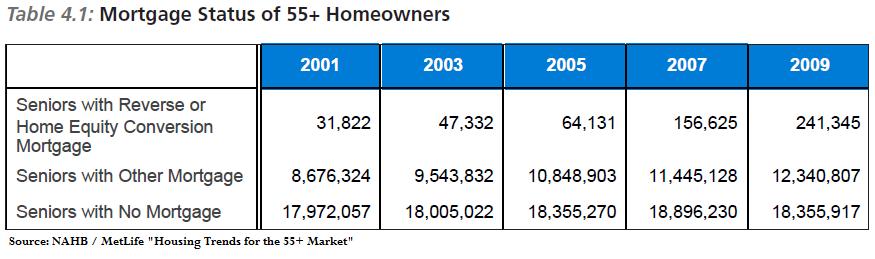

According to “Housing Trends Update for the 55+ Market,” aging baby boomers could soon constitute the majority of American homeowners: “The share of households age 55+ is projected to grow annually, and to account for nearly 45% of all U.S. households by the year 2020.” Based on some rough math, that means that almost half of US homeowners will be eligible for reverse mortgages in 2027. When you consider that only .8% of seniors currently hold a reverse mortgage (compared to 40% with outstanding primary mortgages), it’s clear that the potential for new customers is still vast.

The report also indicated that, “Only 55% of the new age-qualified active adult home buyers who made a down payment reported that it came from the sale of a previous home, significantly down from 92% in 2007.” Due both to the drop in housing prices and the economic recession, almost half of senior homebuyers are being forced dip into savings when purchasing a new home. This phenomenon would seem to imply further potential for growth in reverse mortgages for purchase loans.

Some other interesting factoids include the following: the average reverse mortgage borrower is 77 years old and comes from a household with 1.7 persons. They are unlikely to hold a Bachelors Degree and are typically white. The average property value is $225,000 Average household income for reverse mortgage borrowers was reported to be only $35,000, significantly below their mortgageless peers and also well below those with outstanding mortgages. For better or worse, this shows that the majority of reverse mortgage borrowers would appear to be under genuine financial strain and probably exhausted all of their other options before turning to reverse mortgages.

Finally, “reverse mortgage borrowers and seniors without mortgages stayed in their homes much longer, 24 and close to 27 years respectively, compared to 55+ homeowners who are still paying down their mortgage, 15.6 years.” This would seem to validate reverse mortgages, insofar as they enable seniors that have a sentimental attachment to their homes to continue living in their homes.

In short, I think that the NAHB report painted an optimistic portrait of the reverse mortgage. The figures it provided are consistent with the reverse mortgage surveys that revealed a high degree of borrower satisfaction. In addition, the aging of the baby boom generation, combined with the financial peril of the last few years should ensure that borrower demand for reverse mortgages should remain strong for the immediate future.

Have Feedback on This Article?