According to a recent study conducted by HUD, more than 50% of HECM reverse mortgages are terminated within 6 years of their origination. For older borrowers, the average is closer to 5 years. That’s pretty incredible when you consider that even the reverse mortgage industry recommends that borrowers should plan to remain in their homes for at least 8 more years before a reverse mortgage becomes economical.

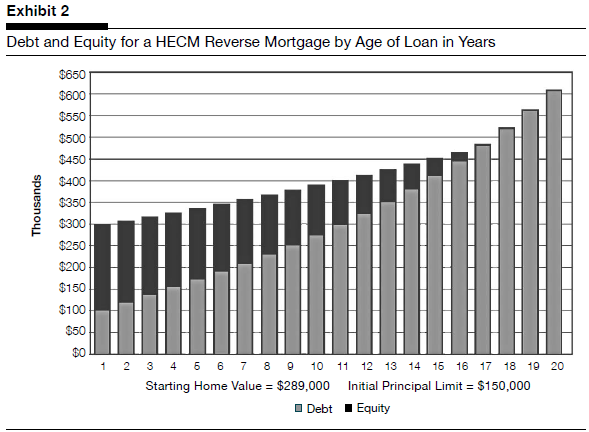

First of all, let’s examine why that’s the case. In a nutshell, the origination fees, closing costs, service fee set-aside, and upfront insurance premium can consume 10% of the loan, before any funds have even been distributed to the borrower. If you allocate all of those fees over a long enough time period, they become infinitesimal on an annual basis. If, however, you terminate the loan within a few years, you are effectively paying 2-3% annually, on top of the 5% interest that you are also being charged. If you don’t think that adds up, take a look at the chart below (courtesy of the HUD report) which shows how reverse mortgages erode home equity (via the proportion of debt to equity).

Back to the subject at hand, it’s unclear as to why such a large portion of reverse mortgages are terminated relatively soon after they are obtained. Regardless, it’s important that when you obtain a reverse mortgage, you make a reasonable estimate of the number of years that you intend to remain in your home (during which the loan will presumably remain outstanding). Think of this as a form of budgeting; based on your estimate (and the chart above, which can theoretically be personalized by your reverse mortgage counselor/lender), you will be able to see how much cash you will have left over after the loan is repaid and you move out of your property. (Bear in mind that the chart also builds in home-price appreciation, and without such appreciation, your equity will be eroded at an even faster rate).

In theory, it’s possible to beat the system if you remain in your home until your death. In practice, though, it’s likely that you will be forced to vacate your residence prematurely (due to health reasons), or will voluntarily choose to move in order to be closer to friends, take advantage of more suitable climate, and.or downsize into a smaller house. In this case, you should consider the potential impact on your equity position and budget accordingly, before obtaining the reverse mortgage.

3 Responses to “Most Reverse Mortgages Terminated within 6 Years”

Have Feedback on This Article?

June 16th, 2010 at 2:10 pm

I wonder if the Congressional Budget Office that came up with the absurd estimates of teh HECM program needing a subsidy know aboutthis. I’m guessing not becaus eif six years is really the average for termination, I’m guessing that there are an exteremely low amount of claims at all.

August 10th, 2010 at 9:17 pm

Actually, lender insurance claims have been surging in recent years, but this is probably less due to over-borrowing than to declining home values. In this sense, the average duration of loans doesn’t bear too significantly in the solvency of the FHA and its need for a subsidy.

July 1st, 2012 at 10:26 pm

This seems like a pretty nasty instrument; selling a home with equity in it and investing the loan funds in laddered CD’s and keeping funds for the time to the first CD payment, and renting seems like a smarter way to go than this.

It seems to play on emotions and charge exorbitant fees to accomplish less than what could occur with simply selling a home which has equity in it.