According to a recent survey by LendingTree.com, the majority of borrowers do not shop around before obtaining a mortgage. Given that a reverse mortgage is a standardized product, insured by the FHA and regulated by the Federal Reserve – reverse mortgage borrowers can be excused for having the same mentality. Ultimately, this is a big mistake, and prospective borrowers would be wise to query a few lenders before obtaining a reverse mortgage.

In terms of selecting an HECM lender, you should begin by asking friends and families for referrals, and or contacting any brokers or loan officers with whom you already have a relationship. [(For the minority of borrowers that plan to obtain a proprietary (i.e. jumbo) reverse mortgage, bear in mind that the number of lenders is quite small].If this is not an option, you can use our Reverse Mortgage lender listing, which is organized by state. You should also consult the lender database of the National Reverse Mortgage Lenders Association (NRMLA), the main industry association, whose members include almost all reputable reverse mortgage lenders. Finally, you can search the Federal Department of Housing and Urban Development (HUD) database of HECM lenders. You should only deal with those lenders that have state licensing and are approved by the FHA.

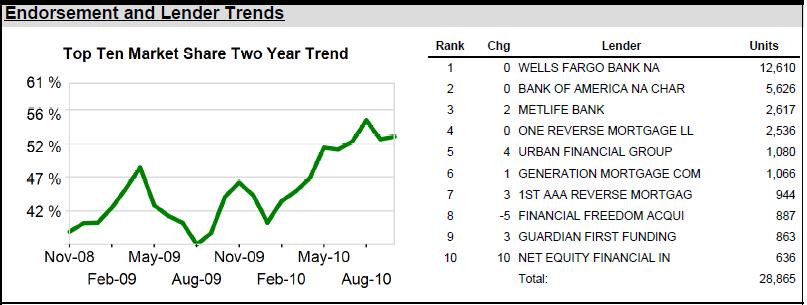

The first major decision is whether you want to deal with a large (national) lender or a small, community lender. In theory, all reverse mortgage lenders offer an identical loan, but the level of service and some of the fees can differ meaningfully from lender to lender. The benefit of dealing with a smaller lender is that you may be able to establish a closer relationship with your loan officer, whereas a national lender might be able to offer you the best deal. According to Reverse Mortgage Insight, Wells Fargo and Bank of America are the two dominant lenders, and the Top Ten Lenders are increasing their dominance of reverse mortgage lending.

At this point, you can start to make contact with specific lenders. Fortunately, reverse mortgage lenders have no reason to pull your credit report, and your credit will not suffer from obtaining quotes from multiple lenders. You should confirm that your lender is willing to offer you the lowest available fixed interest rate (currently set at 5% by the FHA) or a low margin in the case of a variable rate reverse mortgage (~2.25% for HECM Standard and ~2.75% for HECM Saver). Next, you should verify the lender’s fees and other closing costs, and ask if they can waive any fees and/or provide a discount.

Next, you should ask each lender for an explanation of the risks associated with your reverse mortgage as well as any recommended alternatives. If you are already well-informed, you probably won’t learn anything new from this kind of inquiry. Rather, it represents a rudimentary method for gauging the the honesty of your lender. If he pays short shrift to the risks and alternatives, it might be signal that he is incentivized to sell you a reverse mortgage, and any advice he offers is therefore dubious. Along the same lines, you should confirm that you will not be required to purchase other financial products (such as an annuity) in conjunction with your reverse mortgage. This practice is extremely disreputable and often illegal!

After comparing fees, rates, and service, you are ready to make a decision. Don’t feel pressured to choose a specific lender, for whatever reason. And remember that if after obtaining a reverse mortgage you suddenly have regrets, you have 72 hours to exercise your Right of Rescission. In this case, you can either start from scratch with a different lender, or simply forgo obtaining a reverse mortgage altogether.

Have Feedback on This Article?