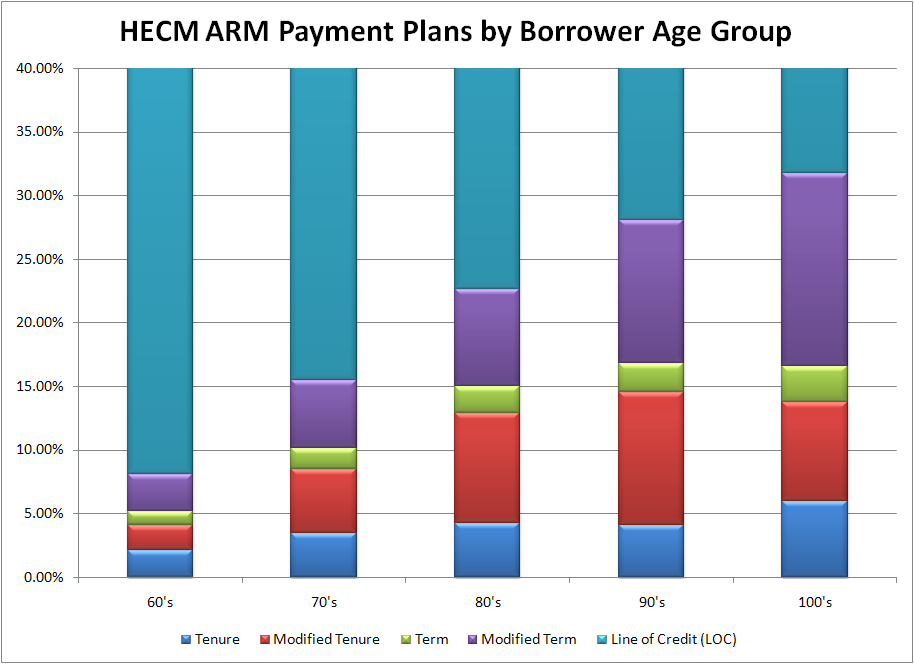

A picture is worth a thousand words, or in this case, a chart is worth a thousands words. Did you ever wonder how borrowers in your age group opt to receive their reverse mortgage payments? Below I’ve pasted a chart from Reverse Market Insight (a provider of analytics for the reverse mortgage industry) which provides a snapshot answer to this very question.

{kind=link}

From this chart, you can clearly see how borrower preferences for payment plans vary by their age. Newly eligible borrowers overwhelmingly prefer to receive their proceeds as a Line of Credit (LOC). [It’s unfortunate that the data isn’t broken down along these lines, leaving us to speculate whether Lines of Credit are really Lines of Credit or whether they are actually lump-sump payments in disguise]. Older borrowers, in contrast, tend to select term/tenure payout plans. However, you can see that regardless of age, borrowers tend to take these in combination with Lines of Credit, rather than receive term/tenure payments in isolation.

For those of you who are scratching your heads, let me take a step back. When you obtain a reverse mortgage, you must decide how the loan will be paid out. If you elect to receive a Line of Credit, you can withdraw the balance of the loan in increments and at times of your choosing. You can take out all of the cash upfront as a lump-sum payment, or withdraw it in installments until the LOC is depleted. With tenure, you will receive a fixed monthly payment (determined by the lender based on actuarial assumptions) until you pass away. A term payout similarly refers to fixed monthly payments, for a duration or at a size of your choosing. With modified term or modified tenure, you will receive term or tenure payments, respectively, as well as a Line of Credit.

Back to the chart, it makes sense that youngish borrowers would prefer the Line of Credit payout option, because this is the most flexible. Many of these borrowers obtain reverse mortgages in order to pay off primary mortgages or for emergency purposes, in which case they would probably withdraw a majority of the loan balances upfront. Those that desire to simply maintain a high standard of living would also be best served by a Line of Credit, because it is conducive to withdrawing cash for discretionary purchases.

Homeowners in their 80s or 90s are both more financially conservative and in worse financial shape than their younger counterparts. Thus, these reverse mortgage borrowers usually select term/tenure payouts in order to pad their monthly incomes. Such borrowers are unlikely to obtain cash for emergency reasons and are even less likely to obtain loans to enhance their standard of living. Still, it’s interesting that these borrowers elect to set aside some cash in the form of a Line of Credit, which can be tapped in an emergency situation or drawn down gradually if the monthly payment was set too low.

While this chart is certainly useful for borrowers that are currently contemplating obtaining reverse mortgages, you should ultimately select a payment plan not based on what others are doing, but based on your own circumstances.

Have Feedback on This Article?