In a recent TV program and accompanying article, CBS News recently reported on the virtues of the HECM Saver. While CBS was right to praise this latest addition to the HECM reverse mortgage series of products, it praised it for the wrong reasons. Sadly, its news coverage demonstrated a serious lack of understanding of the HECM Saver.

The Home Equity Conversion Mortgage (HECM) Saver was introduced in late 2010 by the FHA in response to criticisms that the existing product, the HECM Standard, was not economical for most borrowers. With the HECM Saver, the expensive upfront mortgage insurance premium was effectively eliminated (though the annual insurance premium was left in place). To compensate for the increased risk and to minimize the chance of default, the FHA also reduced principal limits for the new product.

According to CBS News, you can now save money on interest when you obtain a reverse mortgage. This is wrong on two accounts. First of all, while it’s true that mortgage rates are at record lows, the FHA has mandated an interest rate floor for fixed-rate reverse mortgages at 5%. Second, the HECM Saver often carries a slightly higher rate of interest (for both fixed and variable rates) than its counterpart, the HECM Standard, undoing some of the savings from a lack of upfront insurance premium.

CBS News’ second mistake was to advise borrowers to “Consider the loan to fill short-term needs.” This was predicated on the assumption that other “fees are waived,” but this is hardly a given. In addition, while the lack of upfront insurance premium means that reverse mortgages are cheaper than before, they still carry significant upfront costs, exceeding 5% of the value of the loan. The only way such costs can be rationalized is if the reverse mortgage remains outstanding for many years. When you factor in the annual insurance premiums, service fees, etc., a reverse mortgage will almost always be more expensive than other types of loans. A Home Equity Line of Credit (HELOC), for example, is probably a better choice for borrowers with short-term needs.

Ultimately, the HECM Saver was created not for the benefit of borrowers with short time horizons, but rather for borrowers with smaller capital needs. Those that don’t require massive loans, but otherwise are well suited for the HECM Standard, would be wise to consider it. For all other borrowers, a reverse mortgage of any kind should continue to be thought of as a last resort only.

A recent survey sponsored by the National Reverse Mortgage Lenders Association (NRMLA) suggests that reverse mortgages are the panacea for senior citizens’ financial problems. While there are reasons to be skeptical of the survey (because of who funded it) there are also reasons to stand behind it and ponder its implications.

The poll was conducted on behalf of the NRMLA by Marttila Strategies. It involved 1,800 seniors and their adult children and was titled “The Retirement Abyss: America’s Seniors’ Search for Security.” According to the survey, “one-in-four seniors believe they will not be able to cover their monthly expenses in retirement, such as housing and utilities, and nearly 20 percent believe that, without additional cash flow, they will have to give up their homes.” In addition, a whopping 85% of those polled were pessimistic about the state of the economy, and 50% worry about supporting themselves in retirement. This is supported by current economic data, which show rising poverty rates among the elderly.

The survey also established that 80% of seniors want to keep their homes. This jibes with a similar survey conducted by the Joint Center for Housing Studies of Harvard University, which found that, “95 percent of seniors surveyed over the age of 75 want to remain and age in their home.” This presents an obvious conundrum: seniors want to remain in their homes, but lack the cash to do so.

Enter the reverse mortgage…

According to the survey, “74% of reverse mortgage borrowers in the survey described their use of a reverse mortgage as a positive experience. Seniors in the survey expressed that they understood the financial terms of the product very well (75%) and ninety percent felt no sales pressure as part of the reverse mortgage process.” That would seem to rebut the claims of reverse mortgage critics, who continue to insist that reverse mortgages are poorly understood and inappropriate for most borrowers.

On the other hand, the survey also inadvertently confirmed these criticisms, since more than one quarter of all borrowers was either unhappy with or didn’t adequately understand the product’s financial terms. What this probably means in practice is that many borrowers either failed to properly investigate or simply overlooked the high upfront costs and rapid accrual of interest, until they went to repay their reverse mortgages and/or discovered that their home equity had been vastly depleted. These borrowers would no doubt be unlikely to recommend reverse mortgages to other borrowers.

Nonetheless, while the industry could certainly do more to discourage unsuitable borrowers from obtaining reverse mortgages, it deserves credit for the high rates of satisfaction among existing borrowers. For those that meet certain criteria, reverse mortgages can seem like a windfall. As one borrower summarized, “Why on earth aren’t more people telling seniors about this Federally Insured Reverse Mortgage?”

This is my second post in my coverage of the widely circulated Consumers Union report entitled, “Examining Faulty Foundations in Today’s Reverse Mortgages.” In this post, I want to examine the section “Reverse Mortgage Pitfalls” as part of a broader examination of the risks surrounding reverse mortgages.

The report identifies a handful of specific pitfalls. First, there are suitability concerns; namely, reverse mortgages aren’t appropriate for a significant portion of eligible borrowers. According to Consumers Union, “The right reverse mortgage may be appropriate for some low-income relatively healthy seniors who lack other retirement assets, do not qualify for lower-cost alternatives and cannot meet their current mortgage obligation.” On the other hand, those whose health is questionable and/or have definitive plans to move into an assisted living facility at some point should probably avoid reverse mortgages.

Second, there are concerns over the disbursement of and use of the reverse mortgage proceeds. Some borrowers withdraw the maximum amount of equity because they think they should, rather than leaving it in a line of credit account to accumulate interest. Many borrowers also make the mistake of treating reverse mortgage proceeds as a windfall – when it is really a loan – and spend it on frivolous or lifestyle purchases, rather than on necessary living expenses.

Third, many borrowers fail to fully understand the costs of the reverse mortgage because they are deducted from home equity rather than paid directly by the borrower. Along these lines, they fail to appreciate that upfront costs are substantial, and that combined with the compounded interest on the negatively amortizing loan, their home equity may deplete itself in 10-15 years or less.

Next, some borrowers also fail to realize that a reverse mortgage can affect their eligibility for certain government benefits, such as social security and medicaid. According to Consumers Union, “A ‘lump sum’ reverse mortgage payout will immediately put the elder above the asset limit for SSI/Medicaid and disqualify the senior for these important benefits, unless careful legal planning is done to avoid this result.” Before obtaining a reverse mortgage then, all prospective borrowers should research the impact on the money they expect to receive from government entitlement programs.

Finally, due both to deceptive marketing and an inherent lack of understanding, borrowers fail to grasp that a reverse mortgage is a loan agreement, and violating the terms could result in foreclosure. For example, unlike with a conventional mortgage, reverse mortgages do not require the funding of escrow accounts to pay property taxes, hazard insurance premiums, and for routine home maintenance. It is vital that borrowers understand that neglecting to make these payments (out-of-pocket) could trigger a default on the loan and even foreclosure.

For additional information, I would encourage you to consult the Consumers Union report, and to read a couple related posts that I wrote earlier, here and here.

Consumers Union, the non-profit publisher of the Consumer Reports magazine series, recently released a stinging report entitled, “Examining Faulty Foundations in Today’s Reverse Mortgages.” I will address the report in its entirety in a later post, but for now, I would like to focus exclusively on the section on reverse mortgage alternatives.

The report jibes with the advice that I have proffered on this website, and advises that, “Reverse mortgages are very expensive loans, and as such, they should be considered only as a last resort.” Accordingly, Consumers Union recommends that prospective borrowers “should first determine if he or she qualifies for less expensive programs…including Supplemental Security Income (SSI), Medicaid, prescription drug discount programs, energy and telephone discount programs, City and County grants and low-cost home improvement loans (sometimes called “single purpose” loans), state property tax postponement programs, In-Home Supportive Services, and Veterans pensions to pay for in-home care.” The report includes a reference to HECM Resources, a fantastic website with a comprehensive listing of reverse mortgage alternatives, organized by state.

Consumers Union also devotes considerable space to so-called Family Financing. Just as it sounds, this involves a loan from family members (or friends) to the homeowner in lieu of a reverse mortgage. The advantages of this kind of reverse mortgage are primarily financial. Even if the family member(s) charge a comparable rate of interest on the loan, the absence of insurance premiums, origination fees, service fees, and other closing costs will yield significant cost savings over the life of the mortgage, which means there is more home equity left over if/when the home is ultimately sold. Since the loan lacks insurance, however, there are downside risks. Namely, if the home equity falls below the balance of the the reverse mortgage, the lending family member will have no way to collect the difference. Depending on how this is resolved, this could lead to awkwardness and even resentment.

There are a handful of other alternatives that the report doesn’t explore. Common-sense possibilities include consuming less and saving more, retiring later, and/or downsizing into a smaller home. Prospective borrowers can also cash in life insurance policies or borrow from retirement accounts. More complicated solutions include HELOC loans, single-purpose reverse mortgages, and even products that forgo home appreciation in return for a one-time payment to the homeowner.

For those borrowers that are determined to obtain a reverse mortgage, you should consider that you still have options. There are HECM Saver loans and HECM Standard loans, fixed-rate loans and variable-rate loans, loans that disburse all of the proceeds upfront and loans that make term/tenure payments over the life of the life. The point is simply to understand all alternatives (both aside from and within reverse mortgages) and make an informed decision.

I have already reported at length (“Fed Recommends Enhanced Reverse Mortgage Disclosure“) on the Federal Reserve’s attempt to enhance the regulatory framework governing reverse mortgages. As it turns out, the proposed regulation has been met with protests by consumer groups, and may require some fine-tuning before it becomes law.

“A coalition of consumer advocacy organizations…consisting of the Center for Responsible Lending, the National Consumer Law Center, the National Association of Consumer Advocates, the California Reinvestment Coalition, the National Fair Housing Alliance, Consumers Union, Consumer Action, the Neighborhood Economic Development Advocacy Project and the National Community Reinvestment Coalition,” has attacked a few specific components of the proposed regulation.

The first source of contention is a loophole in the rule that prevents cross-selling of financial products. Under the original proposal, lenders would have been barred from requiring borrowers to purchase additional financial products (namely annuities and life insurance policies). However, the guideline has since been revised to allow cross-selling, as long as it takes place more than 10 days after the loan is closed. While this would theoretically still make cross-selling difficult, in practice it could easily be circumvented.

The second problem was a change in the Right of Rescission rule, which gives borrowers the right to cancel their reverse mortgage for any reason within 3 days of obtaining it, and to restructure/refinance a reverse mortgage within 3 years if it was determined that the lender misrepresented the costs. Under the revised rules, the 3-year Right of Rescission would be either eliminated altogether, or the language would simply be altered to make it more difficult for borrowers to exercise this right. The result, argues the Coalition, is that lenders will be disinclined towards accuracy when selling reverse mortgages.

Finally, the Consumer Financial Protection Bureau, which was recently created and vested with the power to study and regulate reverse mortgages (among other things) would see its power and influence vastly eroded by the Federal Reserve’s proposed guidelines. As a result, the Federal Reserve Board would be the only quasi-government body keeping watch over the industry.

There are a handful of other criticisms and suggestions which were put forward during the 90-day comment window. (You can view them in their entirety here). The Fed now has an indeterminate period of time to review these comments and make further revisions.

I’m monitoring the situation closely and will try to provide regular updates.

According to a recent survey by LendingTree.com, the majority of borrowers do not shop around before obtaining a mortgage. Given that a reverse mortgage is a standardized product, insured by the FHA and regulated by the Federal Reserve – reverse mortgage borrowers can be excused for having the same mentality. Ultimately, this is a big mistake, and prospective borrowers would be wise to query a few lenders before obtaining a reverse mortgage.

In terms of selecting an HECM lender, you should begin by asking friends and families for referrals, and or contacting any brokers or loan officers with whom you already have a relationship. [(For the minority of borrowers that plan to obtain a proprietary (i.e. jumbo) reverse mortgage, bear in mind that the number of lenders is quite small].If this is not an option, you can use our Reverse Mortgage lender listing, which is organized by state. You should also consult the lender database of the National Reverse Mortgage Lenders Association (NRMLA), the main industry association, whose members include almost all reputable reverse mortgage lenders. Finally, you can search the Federal Department of Housing and Urban Development (HUD) database of HECM lenders. You should only deal with those lenders that have state licensing and are approved by the FHA.

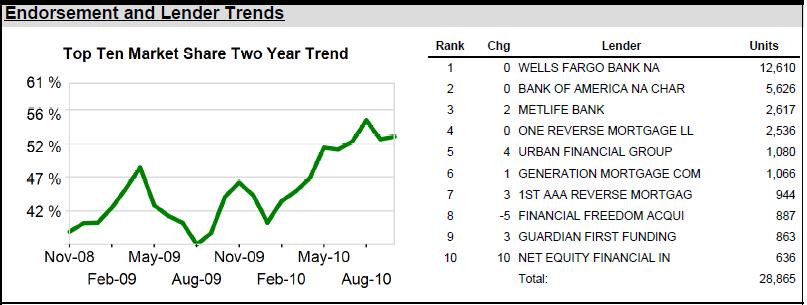

The first major decision is whether you want to deal with a large (national) lender or a small, community lender. In theory, all reverse mortgage lenders offer an identical loan, but the level of service and some of the fees can differ meaningfully from lender to lender. The benefit of dealing with a smaller lender is that you may be able to establish a closer relationship with your loan officer, whereas a national lender might be able to offer you the best deal. According to Reverse Mortgage Insight, Wells Fargo and Bank of America are the two dominant lenders, and the Top Ten Lenders are increasing their dominance of reverse mortgage lending.

At this point, you can start to make contact with specific lenders. Fortunately, reverse mortgage lenders have no reason to pull your credit report, and your credit will not suffer from obtaining quotes from multiple lenders. You should confirm that your lender is willing to offer you the lowest available fixed interest rate (currently set at 5% by the FHA) or a low margin in the case of a variable rate reverse mortgage (~2.25% for HECM Standard and ~2.75% for HECM Saver). Next, you should verify the lender’s fees and other closing costs, and ask if they can waive any fees and/or provide a discount.

Next, you should ask each lender for an explanation of the risks associated with your reverse mortgage as well as any recommended alternatives. If you are already well-informed, you probably won’t learn anything new from this kind of inquiry. Rather, it represents a rudimentary method for gauging the the honesty of your lender. If he pays short shrift to the risks and alternatives, it might be signal that he is incentivized to sell you a reverse mortgage, and any advice he offers is therefore dubious. Along the same lines, you should confirm that you will not be required to purchase other financial products (such as an annuity) in conjunction with your reverse mortgage. This practice is extremely disreputable and often illegal!

After comparing fees, rates, and service, you are ready to make a decision. Don’t feel pressured to choose a specific lender, for whatever reason. And remember that if after obtaining a reverse mortgage you suddenly have regrets, you have 72 hours to exercise your Right of Rescission. In this case, you can either start from scratch with a different lender, or simply forgo obtaining a reverse mortgage altogether.

Since your credit history and personal financial situation are not examined when applying for a reverse mortgage, the only real obstacle is an inadequate level of home equity. That’s because reverse mortgage borrowers must use the proceeds from the reverse mortgage first to pay off any primary mortgage debt. (Of course, those without any primary mortgage debt need not worry about this provision).

If you have significant (i.e. loan balance exceeds 50% of the value of your home) primary mortgage debt, you should consult HUD Principal Limit Factors. This is a table of HUD-mandated principal limits, broken down by age and interest rate, and expressed as a percentage of the value of your home. The principal limit will also vary depending on which type of Home Equity Conversion Mortgage (HECM) you wish to obtain. HECM Standard reverse mortgages carry higher principal limits than HECM Saver reverse mortgages, but require a significant upfront insurance premium.

To determine the maximum amount that you are eligible to borrow, simply scroll down to “5% Interest Rates,” and find the percentage listed next to your age. For HECM Standard loans, the principal limit varies between 61.9% and 77.6%, depending on your age. For HECM Saver loans, the range of principal limits is 52.3% to 61.0%. You will notice that as your age increases and the interest rate declines, the amount of cash you can potentially receive increases proportionally. However, since the current HUD-mandated interest rate floor is 5%, all values below 5% show the same principal limits.

When considering your eligibility, you should take the loan limit and subtract 7% (5% for HECM Saver Loans), which is a conservative estimate of the total closing costs, origination fee, upfront insurance premium, and Service Fee Set Aside (SFSA). If your primary mortgage debt exceeds this figure, you are not eligible to obtain a reverse mortgage.

Due to falling home prices and proportionally declining home equity, this is unfortunately a situation that nearly half of all homeowners will find themselves in. The only immediate solution is to use some of your savings to pay down your primary mortgage debt until it falls below the concomitant HUD principal limit. Otherwise, you can wait a few years under the hope that home prices (and your home equity) will rise or interest rates will fall. (Regardless of what happens, the maximum loan amount will automatically increase by .2-.4% for every year that you age).

Unless HUD raises the principal limits (which is unlikely given the program’s recent financial troubles), you might find yourself sadly shut out of the process.

It seems that there is some confusion regarding the costs associated with a reverse mortgage. In my opinion, this is not the fault of reverse mortgage lenders – though, perhaps they could do a better job in this aspect – but rather do to the very nature of reverse mortgages. Since the initial flow of funds is entirely one-way, borrowers often don’t conduct adequate due diligence and fail to properly understand all of the costs. In any event, allow me to offer some clarification.

The first set of costs are levied when the borrower initially obtains the reverse mortgage. First is the origination fee, which is charged directly by the lender in order to cover overhead and other administrative costs. Generally, this is assessed as a fixed percentage of the value of the home: 2% of the appraised value of the home up to $200,000 and an additional 1% on any portion exceeding $200,000. Then, there are a handful of third-party closing costs, including appraisal fee, credit report, title insurance, recording fee, flood certification, etc. Finally, there is the service fee set aside (SFSA) – $35/month x ~10 years – which the lender will draw from every month for as long as the reverse mortgage remains outstanding. [It should be noted that for promotional/competitive purposes, some lenders will do away with the origination fee and SFSA, and potential borrowers are encouraged to shop around].

Next, the mortgage insurance premium (mip) must be paid to FHA (assuming that the loan is a Home Equity Conversion Mortgage (HECM), as opposed to a proprietary reverse mortgage; this protects the lender (and indirectly, the borrower) from the possibility that the property could one day be worth less than the mortgage balance. With an HECM Standard, the borrower is charged an upfront mortgage premium of 2% of the loan value, whereas the upfront insurance premium for an HECM Saver is basically nil. Borrowers must also pay an annual insurance premium of 1.25% for as long as the reverse mortgage remains outstanding.

The largest (cumulative) cost for all borrowers is interest. Interest is assessed monthly, whether the interest rate is fixed or variable. Since reverse mortgages are always negatively amortizing, the interest is added on the loan balance, and compounds exponentially over the life of the mortgage. If the value of your home doesn’t appreciate at a rate similar to your reverse mortgage rate of interest, then your home equity will steadily erode to the point that it could become negative. If you have aspirations of repaying your reverse mortgage before this point (or even if you don’t!), it’s important to stay abreast of the situation.

Technically, there aren’t any other costs associated with the reverse mortgage. For example, lender consultations and loan counseling are always available free of charge. However, since there is no escrow account associated with the reverse mortgage (unlike with a conventional mortgage), it is imperative that you continue to pay property taxes and hazard insurance premiums, as well as to spend money maintaining the property for as long as you continue to live there. Failure to do so represents a breach of the loan agreement and could trigger termination of the reverse mortgage.

At its annual meeting last month, the National Reverse Mortgage Lenders Association (NRMLA) formally introduced a new level of certification for which members are eligible to apply. Known as the Certified Reverse Mortgage Professional (CRMP), it is intended to designate that a reverse mortgage originator has achieved a certain level of experience, education, and ethics.

According to the NRMLA, “Eligibility to apply for a CRMP designation requires that a loan originator have at least two years of experience and closed 50 reverse mortgages. Only then can they enter the process which includes 12 hours annually of continued education, participating in a three-hour interactive ethics training seminar, a background check and sitting for an exam. The certification is valid for three years, but a designee must recertify every year and obtain 12 hours of continuing education credits annually over that period.” In this way, the certification can serve as a point of competitive distinction. All else being equal, most borrowers would be more inclined to obtain a mortgage from a loan originator that had undergone the maximum level of training and received the highest designation currently bestowed by the reverse mortgage industry association.

From the standpoint of the NRMLA, the certification will not only be a source of income, but will also provide an ethical boost to the reverse mortgage product and to the industry in general. “The program is administered by an Independent Certification Committee comprised of NRMLA members that oversee the establishment of criteria, eligibility, testing and recertification.” In this way, the NRMLA can address claims that reverse mortgage borrowers don’t understand what they are agreeing to and aren’t aware of their other options.

Personally, I think this is a step in the right direction. It’s important that borrowers feel comfortable with their respective loan originators and not have to worry that vital information is being withheld so as to “facilitate” the transaction. By dealing with a CRMP loan originator, there should be a decreased likelihood that borrowers will be cajoled into obtaining a reverse mortgage when the conditions are not suitable. Meanwhile, the handful of professionals that have already been certified will be held to a higher standard, since they represent not only their respective lender, but also the industry at large.

Let’s just hope that the designation proves its worth and isn’t used cynically to lull borrowers into a false sense of security.

According to most surveys, the majority of current borrowers are satisfied with their reverse mortgages and have indicated that their lives are better off because of them. However, the operative word here is current. As Reverse Mortgage Daily concedes, little or nothing is known about how former borrowers feel. As a result, “The most fundamental question about the consumer impact of the HECM has yet to be answered.”

That the majority of current borrowers are satisfied with their reverse mortgages is not altogether surprising. After all, the initial flow of funds is entirely one way. Borrowers sign a few forms, have their homes appraised, and then receive significant sums of money. There are no monthly payments, and the lender will only come calling if the terms of the loan agreement are breached (i.e. if the borrower neglects to pay taxes and hazard insurance premiums, or fails to maintain the property). In the beginning, horror stories are rare, and except in cases of outright fraud – which plague every industry – most loans are originated in a scrupulous manner. How could anyone not be satisfied with such a product?

As for borrowers’ level of satisfaction over the long-term, this is less clear. The immediate impact of a reverse mortgage is necessarily to improve one’s financial situation. If there was an existing primary mortgage, the reverse mortgage eliminated it and any need to make monthly payments. If the primary mortgage had already been paid off, the reverse mortgage borrower will suddenly find themselves with substantially more money. Unfortunately, this is really just an illusion, since these funds ultimately need to be repaid.

Reverse mortgages are always negatively amortizing, which means that principal begets interest, which in turn, begets more interest. In practice, that means that the reverse mortgage loan balance will grow at an exponential rate. Depending on the rate of interest and the initial loan balance (as a proportion of one’s home equity), the loan balance will probably approach (and even exceed) the value of the home after one or more decades. That means that if the reverse mortgage is terminated (whether by the borrower or the lender), the majority of the proceeds from the sale of the home will probably go towards repaying the loan.

Of course, borrowers should understand all of this when they obtain the reverse mortgages and the proceeds are distributed. In practice, however, it’s not known whether borrowers are willing to acknowledge this or actually do understand it. Ideally, reverse mortgage borrowers would continue living in their homes until they pass away, in which case, this wouldn’t be much of an issue. Given that most reverse mortgage borrowers probably have weak financial positions to begin with, having to move out prematurely without any cash or leftover home equity would be nothing short of devastating.

And I think it goes without saying that such borrowers would probably voice regret about having obtained the reverse mortgage in the first place. For all we know, a substantial portion of all borrowers might sing a different tune when they receive the “bill” for the reverse mortgage and are confronted with the reality that the money they received was never free.

The problem is, we just don’t know.